Additional Superannuation Contribution (ASC) was introduced on 1st January 2019, it replaced the Pension Related Deduction (PRD). Whereas PRD was a temporary emergency measure, ASC is a permanent contribution in respect of pensionable remuneration.

Application of ASC

ASC will apply only to individuals who are in receipt of pensionable pay and applies to a person who:

(a) is a member of a public service pension scheme or

(b) receives a payment-in-lieu of pension or

(c) is entitled to an ex-gratia retirement gratuity (annual or lump sum) on retirement

Assessing ASC

Unlike PRD, ASC is only chargeable on pensionable remuneration. Pensionable remuneration includes:

- Basic Pay (excluding non-pensionable overtime) due to the public servant in respect of that period, and

- Allowances, emoluments and premium pay (or it's equivalent) which are treated as pensionable pay

ASC Treatment

ASC qualifies for tax relief but not Universal Social Charge (USC) relief. There is employer PRSI relief in respect of ASC, it does not qualify for employee PRSI relief.

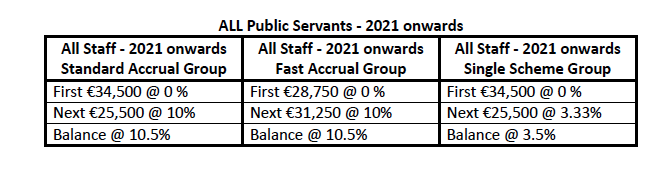

ASC Rates and Thresholds

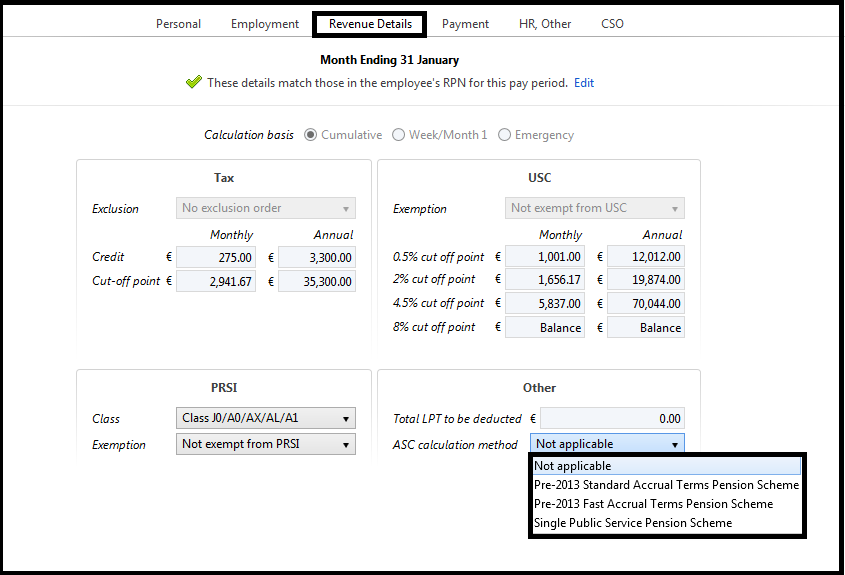

Setting up the ASC Deduction in BrightPay

Go to Employees > select employee to whom the deduction will apply > Revenue Details > Select the appropriate ASC calculation method > 'Save Changes'.

You can choose between the following options

- Pre-2013 Standard Accrual Terms Pension Scheme

- Pre-2013 Fast Accrual Terms Pension Scheme

- Single Public Service Pension Scheme

Payslips

Additional Superannuation Contribution will display separately on the Employees Payslip as ASC under the deductions section.

Comments

0 comments

Article is closed for comments.